How a 25% average return = zero growth

Average returns can be very misleading

Once you begin to filter through the noise generated by the financial media, the plethora of “top” advisors, and financial product salespeople, you begin to see a few common threads.

One of these threads, and the one you’re meant to believe holds together the intricate tapestry of your financial life, is the all important investment return.

The higher the return, the thinking goes, the more money you make.

And the more money you make, well… who would complain about that?

Not so fast…

First of all, no one – let me repeat that… NO ONE – can see the future.

Not Warren Buffett.

Not your financial advisor.

Not the fortune teller at the carnival.

Not me.

Not you.

Not anyone.

And if someone says or implies that they can get in and out of the market at just the right time, or they can pick the perfect investments and avoid the losers… well, they’re lying to themselves, lying to you, or more likely… both.

If you’re attracted to these questionable claims of clairvoyance, I wish you the best.

We don’t serve that here.

Sure, you or your crystal-ball-wielding advisor may just get it right.

For those of you still with me, let’s agree we don’t know what will happen in the future.

We don’t know what’s going to happen in the investment markets just like we don’t know how many days we each have left to make the most of our lives.

So, naturally, we turn to the past.

How did an investment or portfolio of investments do in the past?

Surely, that will be a reliable guidepost to how it will do in the future.

Once again, not so fast…

You may have heard or read the ever-present investment performance disclosure that sounds something like this:

“Past performance is not an indication of future results.”

Below this article is a link to my legal disclosures that includes this exact sentence:

“Past performance is not a guide to future returns.”

And you know what?

It’s true.

If you flip a coin and get 4 tails in a row, you’re next flip still has a 50-50 chance of being a head OR a tail.

You’re not any more likely to get a head after flipping 4 tails in a row.

This is a fact.

However, our brains and our intuition often tell us a different story.

And it’s this same story that many financial advisors rely on to pitch their services to you.

Even if they’re willing to admit that the future is uncertain and unknowable, many are all too willing to treat the past as prologue.

When they do this, they’re no longer acting as your advisor.

They’re instead acting as a reporter.

They’re telling you what’s already happened even though they have no clue what will happen tomorrow.

“But look at the 5- or 10-year average return,” they’ll say.

“See how this investment did in a difficult year like 2008,” they’ll say.

And so, after my long-winded introduction, let me call your attention to the danger of putting any faith in “average returns.”

Here’s a hypothetical investment:

You have a $1 million investment.

In year one, you get a 100% return, so now your investment is worth $2 million.

In year 2, you’re not so lucky, and you experience a 50% loss, so now your $2 million is worth $1 million (again).

You started with $1 million, and after 2 years, you still have $1 million.

You haven’t made any money.

But get this… your average percentage investment return is 25%.

Yep, you read that right.

After 2 years you made no money, but your 2-year average return was 25%.

This is just one example of the trouble with focusing on average returns.

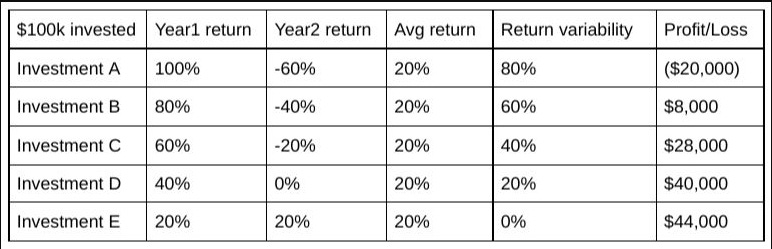

Here’s another example:

The table above shows 5 different investments labeled A through E.

Each of the 5 investments starts with an investment of $100,000.

And each investment has an average 2-year return of 20%.

These investments had results ranging from a $20,000 loss of principal to a $44,000 gain after 2 years.

Clearly, it’s about much more than average returns!

And even if past returns were an indication of your future results (they ain’t), percentage returns and your actual dollar wealth can tell two very different stories.

And remember, you can’t spend percentage returns at the grocery store.

If you have questions about this or would like to get a 2nd opinion on your investments, your retirement plan, and the advice you’ve been getting, let me know.

And here’s a good read - and reminder - from Rubin Miller.

I encourage your to check it out:

Thanks for reading.

Until next Wednesday,

Russ