Do the opposite?

If something's not working for you...

Happy Wednesday,

Today is National Opposite Day.

So if your financial and retirement planning doesn’t seem to have you headed in the direction you want go, perhaps you should consider personally participating in Opposite Day today.

Maybe something like this:

Another way to consider Opposite Day is instead of making one or more New Year’s resolutions, instead make a “quit doing” list.

What are those things that you want to stop doing or remove from your life.

Often it’s easier to realize what we don’t want than to try to put our finger on what it is we do want.

Moving along…

I’ve touched on version 2.0 of the Secure Act recently.

Here’s another resource you might find helpful as you consider the impact of this latest legislation on your own retirement planning:

Many people mistakenly think retirement planning is a math problem.

And certainly, there’s some basic math involved.

But it’s not solely about math or spreadsheets or calculators or software.

Because while math is rational and fact-based, money is emotional and can mean very different things from one person to the next.

I’ve met some people over the years that rely on math and spreadsheets to avoid dealing with the intangible and emotional aspects of money that can lead us to make decisions that aren’t always in our best interest.

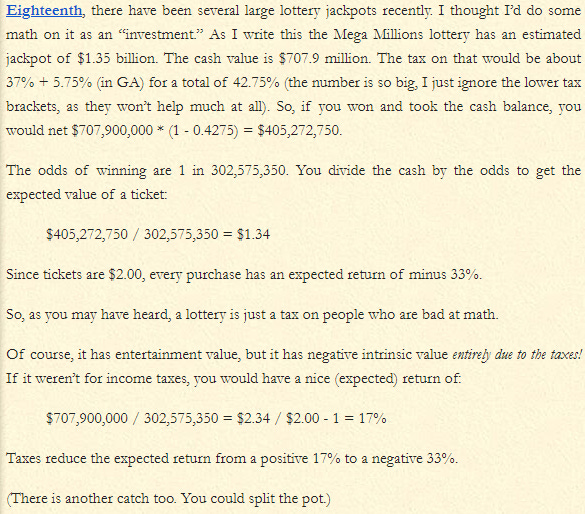

For example, here’s some cold hard math on the recent Mega Millions lottery:

Reading the above paints a pretty clear picture that buying lottery tickets is a losing proposition financially.

But many people - smart, educated people - regularly buy them.

Sort of like seeing nurses and doctors standing outside the hospital on a smoke break as I mentioned a couple of weeks ago.

Additionally, many people mistakenly cling to a false sense of precision in their financial planning.

This is often a result of focusing too heavily on the math.

They rely on their spreadsheets or an advisor’s detailed cash flow projections which presume to know what a person’s expenses (and life) will be 2 years from now.

And 20 years from now.

There’s not a more fitting quote for retirement planning than the words often attributed to John Maynard Keynes but which actually come from Carveth Reed, a British logician and philosopher:

It is better to be vaguely right than exactly wrong.

And as I’ve written many times before, financial planning is the ongoing process of being a little less wrong tomorrow.

So maybe the best retirement plan has a touch of math, a dash of art, and a smidge of luck and/or good timing.

What do you think?

Links & things

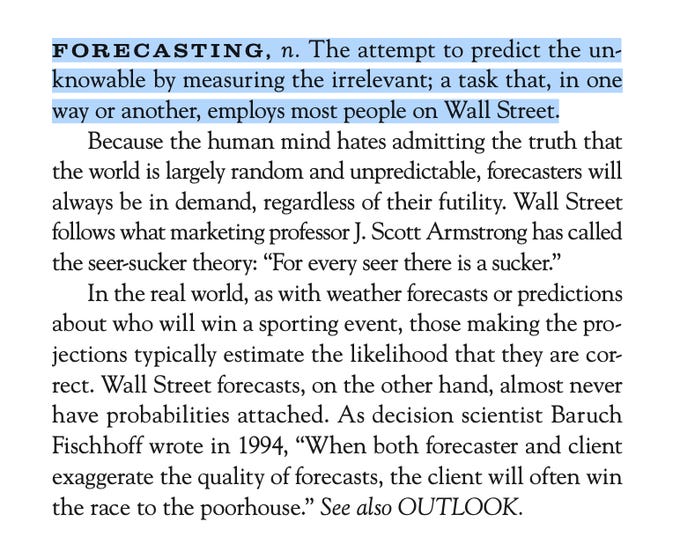

Forecasting

If you know me or have followed my writing for any length of time, you’ll know I don’t make forecasts nor do I pay any attention to others’ forecasts. Here’s a great explanation of why I feel this way:

Stolen

You’re probably familiar with the quote

Comparison is the thief of joy.

Luke Smith expands on this idea - something I agree with - in his recent Humble Dollar article.

Don’t believe me?

Then read this recent Nick Maggiulli article on How Much Income Do You Need to Be Rich?

No matter if you’re still working or have been retired for 10 years, I’m sure you sized yourself up against these income levels to see how you stack up.

I know I did.

And I’m regularly asked by clients how they stack up or compare to my other clients.

But it’s a question without an answer.

Because you’re on your own unique journey.

Your decisions - about money and about life - are influenced by your upbringing and the lessons you learned early in life.

And every day since.

Sure, from a pure math standpoint, it might be interesting to know how your income or net worth compares to others in your age range.

But how do you compare happiness?

Fulfillment?

Contentment?

Food for thought…

Thank You!

I’m grateful to have you as a reader.

If you have any questions or an idea for a future newsletter, blog post, or YouTube video, I'd love your input.

Just hit reply - I read (and truly appreciate) every email you send.

Until next Wednesday,

Russ