How much can I spend if I retire at 62 with $3 million

It's not just about math. It’s about tradeoffs, timing, and how you want to live

Key takeaways

$3 million isn’t the whole story - What you own and how it’s taxed can quietly shape your retirement paycheck more than you might expect.

Your life expectancy changes everything - Planning to live to 84 vs. 104? That one assumption can shift your monthly income by thousands.

Flexibility is your hidden superpower - If you’re willing to adjust your spending over time, your plan becomes a lot more resilient - and a lot less stressful.

The age at which you retire and how much you’ve accumulated for retirement are important numbers, but they’re only part of your retirement plan.

I wrote about 2 important - and different - numbers just last week.

I’m consistently asked some variation of the question above even if the numbers differ from one person to the next.

When you plan to retire and how much you’ve saved up for this next chapter of your life are a great starting point.

But they’re just the start…

I’ve introduced you to my hypothetical client Jane Sample before.

Let’s revisit her retirement income plan to help us think through the question posed above.

Jane is 62 and lives in Florida.

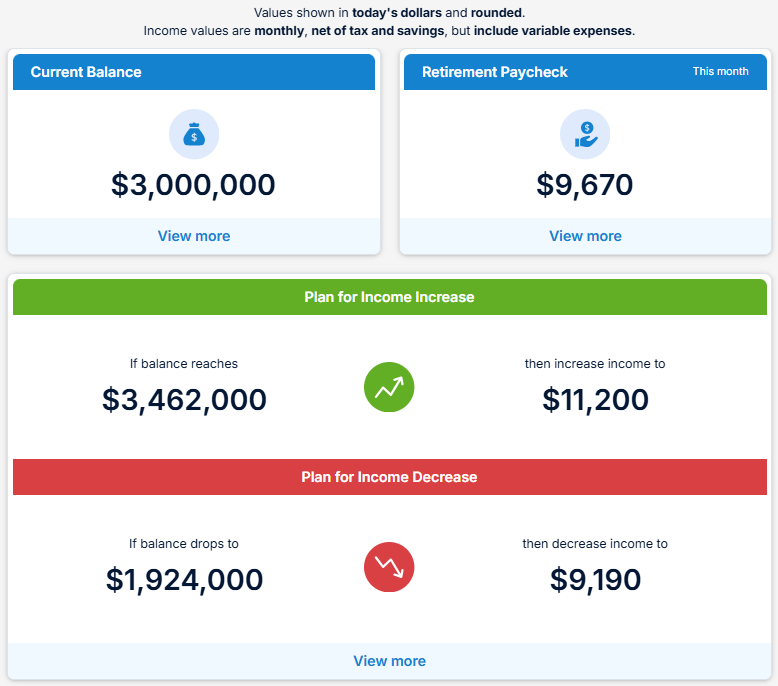

In the screenshot above, you’ll see in the upper-left that her current portfolio balance is $3 million.

And in the upper-right, this analysis indicates that she can spend $10,600 this month.

This is her retirement paycheck.

Note: for purposes of this article, I’m not including any Social Security or other income for Jane. This is an isolated analysis of what her accumulated portfolio assets will confidently provide to her each month throughout her retirement.

Now, let’s dig a little deeper.

What is the composition of Jane’s investment portfolio?

Well, in the numbers above, I’m assuming it’s all in a non-retirement brokerage account with a total account cost basis of $2 million:

If I change the account’s total cost basis to $1 million, thus assuming more unrealized capital gains, you can see the impact to Jane’s 1st monthly retirement paycheck:

The lower cost basis assumption results in approximately $400 less in after-tax retirement spending in her 1st month of retirement.

Taxes matter in your retirement income plan.

But what if taxes didn’t matter?

What if Jane’s $3 million was all in a Roth IRA which means she could spend the money without any income tax liability?

You’ll see above that no income tax liability helps, but maybe not as much as you would have guessed.

Now, what if half of Jane’s portfolio were in a non-retirement account with a cost basis of $750,000 and the remaining $1.5 million was in an IRA?

Again, some impact… but not a life-changing difference:

Where we’ll start to see a meaningful impact to Jane’s retirement paycheck is when we adjust some other critical assumptions in her plan.

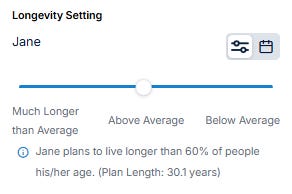

In all of the numbers above, we’ve used this life expectancy assumption for Jane:

This assumes she’ll live longer than 60% of people her age and make it to 92.

But what if we assume she’ll live “much longer than average” and live to just over 100? This means she’ll outlive 90% of people her age.

You can see above how your longevity can impact your retirement paycheck.

On the other hand, what if Jane has a family health history leading her to believe she’ll live well below average or only longer than 30% of people her age?

You can see the impact if she only lives to age 84 below:

None of us know how much time we have left, nor how healthy our remaining years will be.

And while we can do much to influence our health and our longevity, it’s ultimately out of our control.

Nevertheless, it’s worth thinking about, discussing, and incorporating any relevant family and health history into your personal retirement income plan.

Your health and life expectancy can also impact your decision around when to start Social Security benefits, among other things.

But in addition to your longevity, there’s another factor worth your consideration.

It’s your “retirement paycheck risk tolerance.”

This is not your tolerance for investment risk.

Instead, this is your ability and willingness to adjust your retirement income in the future.

I’ve previously covered retirement income guardrails and their importance in creating and maintaining a sustainable retirement paycheck for the rest of your life.

But what I haven’t written about before is your ability to adjust the relationship between your retirement paycheck and your guardrails.

And your flexibility in changing the amount of your retirement paycheck from time-to-time as dictated by your personal plannin guardrails.

In the image above, you can see Jane’s retirement income guardrails.

At the bottom of the image you can see the “Guardrail Settings” slider which I currently have set to the middle of the range.

However, if Jane is willing to accept a lower spending level along with a lower chance of needing to adjust her retirement paycheck, you’ll see in the image below that it expands her personal guardrails:

This means her portfolio balance can fluctuate more before it would trigger a retirement paycheck adjustment.

Though it also means she’ll have to accept a lower retirement paycheck each month.

In statistical terms, the left-most position on the retirement income setting means that Jane will have a 1% chance of overspending and a 99% chance of underspending.

The middle - or default - setting means a 20% risk of overspending and an 80% risk of underspending.

And even the most “aggressive” retirement paycheck setting (to the far right on the slider) indicates a 40% chance of overspending and a 60% chance of underspending.

And the dollar equivalent amount of this range is $10,100 per month on the low end and $13,000 per month on the high end.

So after all these numbers and screenshots and assumptions, what’s the bottom line?

It’s simply this:

Once you know when you want to retire and how much you’ll have saved up for retirement, there are still many details and discussions to explore to further personalize your retirement income plan.

You need to make sure that your plan reflects not just your financial situation and preferences, but also your values, goals, and priorities.

And you should also think about and accommodate your family health history as well as your willingness and ability to adjust your retirement paycheck once you stop receiving a paycheck from your employer.

Taxes and other related details matter.

But it’s the combination of all this information in addition to your input on the life you want to live that truly makes your retirement income plan uniquely yours.

And even after you’ve explored and accounted for everything, your plan will change.

Because life.

If I can help you personalize your retirement income plan, get in touch and let’s discuss it.

Thank you for reading.

If you have any questions or suggested topics, please reply or leave a comment below.

Until next Wednesday,

Russ