Let's Talk Taxes

Do you really understand your income taxes?

Happy Wednesday!

Well, it’s that time of year again…

It seems that every other commercial on TV is a pitch to prepare and file your taxes. Many with the promise of an interest-free “tax refund advance.” 🤦♂️

And it’s only going to continue as we get closer to April 18th, the deadline to file your 2023 taxes (without an extension).

I’m not an accountant or a CPA. I don’t prepare anyone’s taxes, not even my own.

But taxes have always been an important element of the financial planning conversations I have with my clients.

Taxes influence virtually every financial decision you’re making. Either directly or indirectly. Now or in the future.

Over your lifetime, taxes will be one of your largest expenses.

Yet, I find a lot of confusion about taxes among clients and others I talk to.

For instance, I’ve had people tell me they’re worried about getting too big of a bonus because it will push them into a higher tax bracket.

I’ve even heard stories of people declining a promotion and pay raise because it would put them in a higher tax bracket.

Or that the bigger the tax refund, the better.

And don’t even get me started on “writing off” business expenses.

Many folks have no better understanding of business expense deductions than Kramer:

But I’ve got good news…

If you don’t understand every bit of your personal income tax picture, you’re not alone.

I don’t profess to know and understand it all, though I’d like to think I know a little more than the average bear.

One tax tool that I’ve been using for the past few years to help me and my clients better understand their income tax return produces this information:

The above image is an excerpt from a “tax report” I can generate from your tax return. It takes your tax return data and gives you a high level overview and puts things in easier to understand language.

For example, knowing your “marginal tax rate” versus your “average tax rate” can be quite eye opening for many folks.

Your marginal tax rate is the rate you’ll pay on the next dollar you earn.

While your average tax rate is your total amount of taxes paid divided by your total earned income.

Does this type of report provide instant clarity and understanding across your tax return?

No, of course not.

But it’s certainly a step in the right direction.

And the tool that I use to create this report also allows us to run “what if” scenarios around your current and future taxes to help us evaluate the tax impact of different planning and investment decisions.

Things like:

How much of my Social Security will be taxable?

Based on my capital loss carryforwards, can I take some “tax-free” capital gains this year?

If I take more money out of my IRA this year, will that increase my Medicare costs due to IRMAA?

I think it’s well worth the effort to better understand how income taxes work and how they apply to your unique situation.

This is especially important for the women out there dealing with divorce or widowhood.

Now, back to the confusion about taxes above…

In the US, our income tax brackets are progressive.

This means the more you earn, the more tax you’ll pay. But it works a little differently than many people think.

Watch this short, 4-minute Kahn Academy video for a simple explanation:

If your income - whether bonus or salary - pushes you into a higher tax bracket, the higher bracket isn’t retroactive to the first dollar you earned.

So, by all means, get that big bonus or that promotion and pay raise. You’re only paying marginally higher taxes on the dollar amount in the higher bracket.

What about those who look forward to their tax refund every year?

While there’s technically nothing wrong with this and a tax refund can have a positive mental and emotional benefit, what it really means is you paid more tax than necessary throughout the year (most often through payroll deductions) and you’re simply getting YOUR money back after providing an interest-free loan to the IRS.

This can be remedied by adjusting your payroll withholding on a form W-4. Though these days this is often handled online through your employer or payroll provider.

From a purely financial standpoint, you should attempt to reach a “break even” with the IRS meaning you get nothing back and you don’t owe them anything.

Of course, as with all things IRS this is much easier said than done.

Personally, I wind up writing a check to the IRS when I file my taxes most years. This means I’m the one getting an interest-free loan from the IRS. 😉

One local tax note for my fellow Georgians:

On April 26, 2022, Georgia Governor Brian Kemp signed into law HB 1437, which replaces the current graduated personal income tax with a flat rate of 5.49% effective January 1, 2024, with gradual reductions each year until the flat rate reaches 4.99%, effective January 1, 2029.

Source: Ernst & Young

As you begin to assemble your documents and get organized to file your 2023 tax return, hopefully some of the ideas above will help you think about your taxes differently.

In the context of your broader financial and retirement plan.

Any questions about your taxes?

Hit reply and let me know.

For now, I’ll leave you with this…

The difference between death and taxes is death doesn't get worse every time Congress meets.

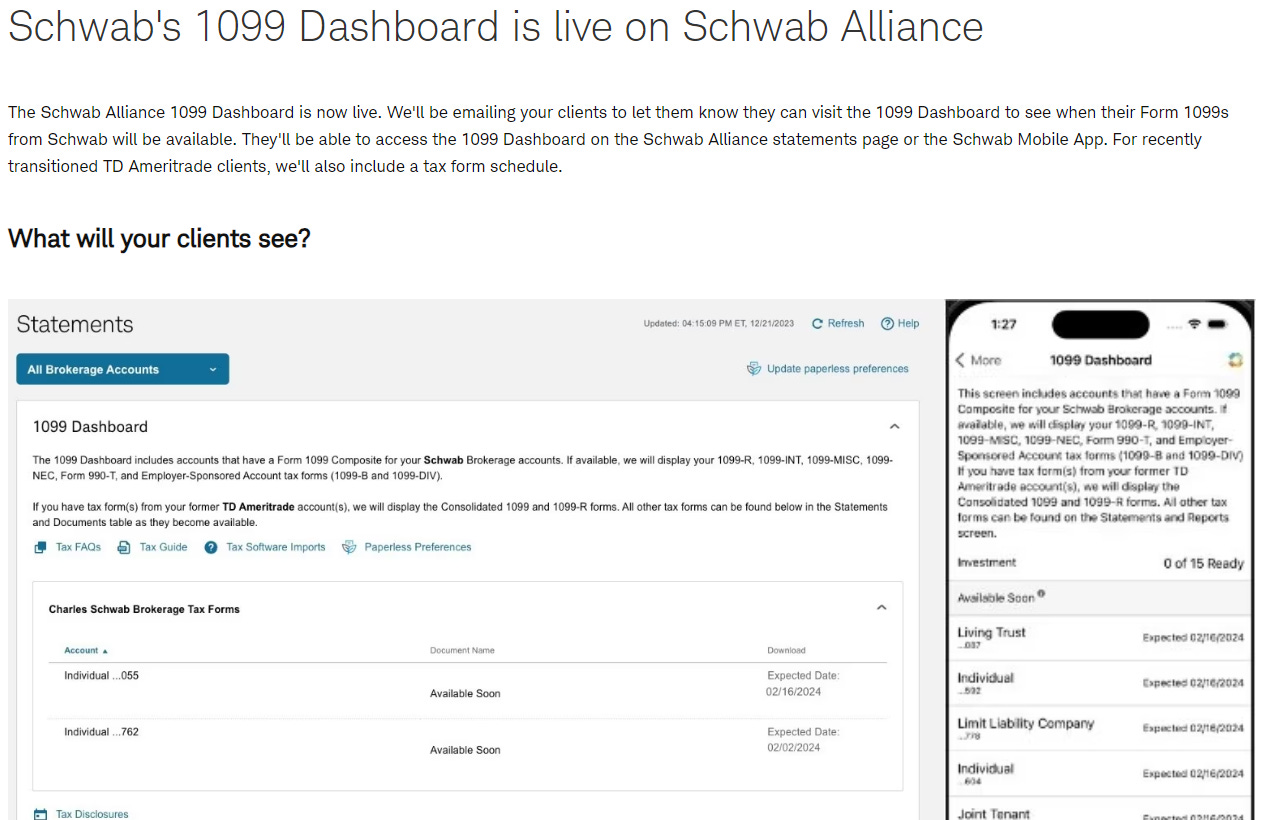

Schwab Tax Documents Update

For those of you who are clients or have accounts at Schwab, you can now login at Schwab.com and check your “1099 Dashboard” to see when to expect your 2023 tax documents to be available.

They’re currently estimating mid-February for most clients.

Thank You!

I’m glad you’re here. And I’m grateful to have you as a reader.

If you have any questions or an idea for a future email letter, blog post, or YouTube video, I'd love your input.

Or if you just want to say hi 👋

Simply hit reply - I read (and genuinely appreciate) each and every message you send.

Until next Wednesday,

Russ

I was forced to retire last year in March. Fortunately, I'm over 65 and had/have money saved up. However, taxes have me concerned. For the first time in my life, I am going to an accountant. Hubby is still working, plus he's federal employee. When he retires, it is going to be "interesting." I am familiar with "offset" but still don't understand how that's going to work for us.