Let's think this through

Good morning!

As we continue to experience the ups and downs in the investment markets, many of you may be wondering if it makes sense to just "sit this out".

It's a good question and one that deserves some attention.

So let's think through this and how it might go...

You have an investment portfolio.

Maybe you're also retired so there's no longer a paycheck which means you're likely not adding to your savings.

All this combined can make the current market environment an anxiety-inducing roller coaster and you're probably thinking,

"I just want to get off this thing!"

Again, that all makes sense.

And if you feel this way, you're not alone.

So, let's say we sell your investments and put it all in a money market fund.

Phew!

That feels better, doesn't it?

But then what?

When do you put your money back into the market?

Based on my 30 years of experience along with countless conversations with clients, other professionals, family, & friends, you'll put your money back into the market "once things calm down."

That's the phrase I've heard most often.

Let's ignore the fact that we don't know if or when things will "calm down."

My question to you, dear reader, is when do you think you'll "feel" like things have calmed down?

Again, based on experience, most people feel more confident as the market rises. In other words, we'll reinvest (maybe) once the market goes back up and feels less risky (or scary).

There are people out there who bailed out after the market dropped in 2008 and have never gotten their money reinvested.

On the surface, you might be a little jealous of these folks.

They didn't have to deal with the 2008 mess, and they're not on this current roller coaster either.

Smart, right?

Well, the numbers paint a different picture:

The chart above (source: Kwanti Analytics) shows the total return of the S&P 500 from January 1st, 2007, through October 5th, 2022. (I'm writing this email on October 6th, FYI)

If you're having trouble reading that chart (click the chart to see larger version) it shows that over this period, the S&P 500 had a cumulative return of 267% and an average annual return of over 8.5%.

These numbers are after the recent market downtrend as you can see in the chart.

Will today mirror what we saw in 2008 and since?

Of course not.

But that doesn't mean there isn't something to take away from history or this imaginary scenario of getting out of the market to soothe your emotional fears (which we all have, by the way) at the potential expense of the cold, hard logic of purchasing power being eroded by inflation over time.

Even when inflation is at levels more in line with history - not the crazy high inflation we're all living with right now.

So, if you get out the market, it's probably going to feel nice short-term.

But if you do get out and you have the discipline to eventually get back in, it will likely be after the market has gone higher which means you'll be selling low and buying high, at least on a relative basis.

That ain't how to do it, folks!

And what about your ability to fund the rest of your life? And your lifestyle? And take care of those who are important to you?

I apologize if this comes across as "preachy" and I'll step down off my soapbox now.

I'd just hate to see you make a short-term decision that could have a lasting long-term impact on your ability to maintain your lifestyle for the rest of your years.

Disagree? Want to talk about it? Have another perspective?

Hit reply and let me know.

Links & things

Medicare's annual open enrollment period opens up here in a few days on October 15th and it runs through December 7th. Whether you're approaching age 65 and signing up for Medicare for the first time or you're already on Medicare and reviewing your coverage and prescription drug plan for the year ahead, please reach out and let's talk about it.

Not only do your health insurance costs factor into your financial planning, but it can be overwhelming for some to face the myriad decisions involved in this important choice.

So please get in touch (or just hit reply) if you'd like to talk about it. I have several resources I can bring to the table to help you make a smarter, more informed decision.

And this is an important area where I've been getting more and more involved with my clients.

Speaking of Medicare:

What makes a happy retirement?

Having enough money certainly helps, but I think we can all agree there's more to life (and retirement) than money:

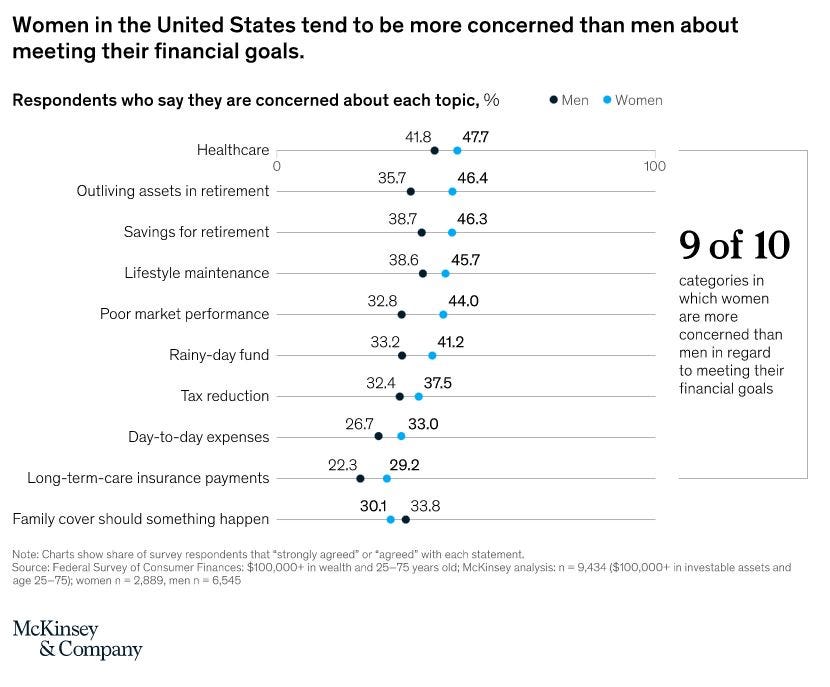

And while everyone has their own challenges and concerns when it comes to their financial future, the chart (click chart to view larger version) below from a recent McKinsey study points to the fact that women are generally more concerned than men are:

Thank you, as always, for reading.

And if you have any questions or an idea for a future newsletter, blog post, or YouTube video, I'd love your input.

Just hit reply - I read (and appreciate) every email you send.

Until next Wednesday,

Russ