Retirement planning in pictures

A visual guide to the challenges (and opportunities) as you plan for retirement

Hope your Wednesday is wonderful!

Today, I’m going to outline retirement planning with a few visuals…

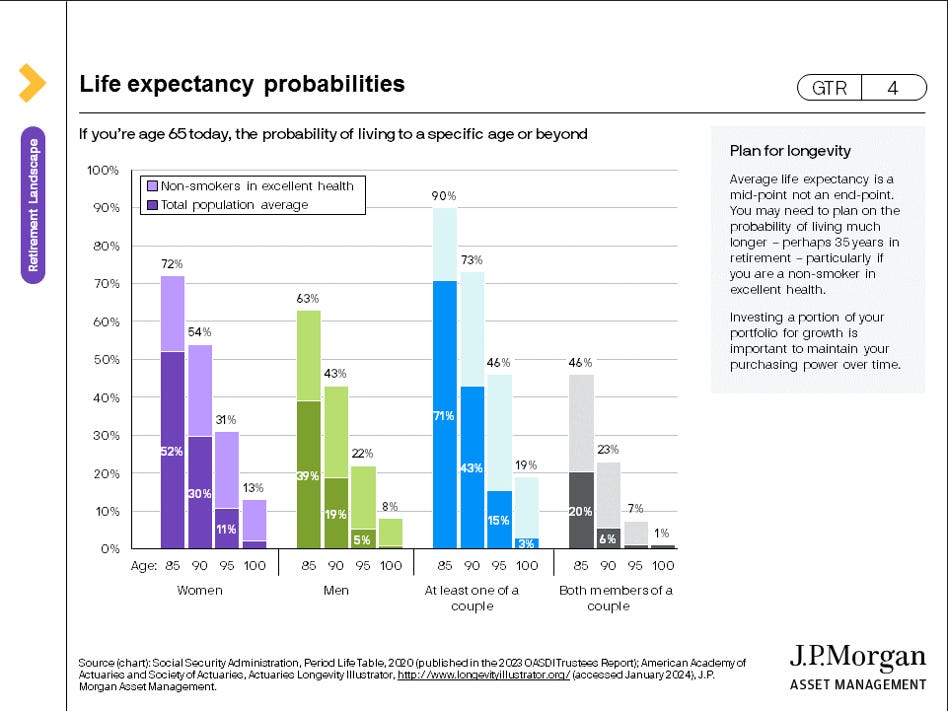

Life expectancy

Retirement planning would be much simpler if we knew how long we’re going to live.

But we don’t.

And to further complicate things, we don’t know how healthy we’ll be as we age, though we do have some level of control over our health and wellness.

And note the sidebar in the slide above: the figures above are averages and you could live much shorter or longer than the ages in the chart.

Which is why it’s important to live a great life today while also being well prepared for an uncertain future.

Well-being

As I’ve written before, I think the best mindset as you approach retirement is to have something to look forward to.

Instead of retiring to get away from work, why not retire to more time with family and friends.

Retire to more volunteering.

More golf or tennis or pickleball.

More involvement with your church or your community.

Many people are unprepared for the void in their lives once they stop working.

They stumble into retirement just happy to be done with work only to find they have no idea how they’ll fill the 8+ hours they spent working every day.

Or how they’ll replace the social connections with coworkers established over decades in some cases.

Retiring well isn’t just about money.

It’s also about mindset.

Retirement income

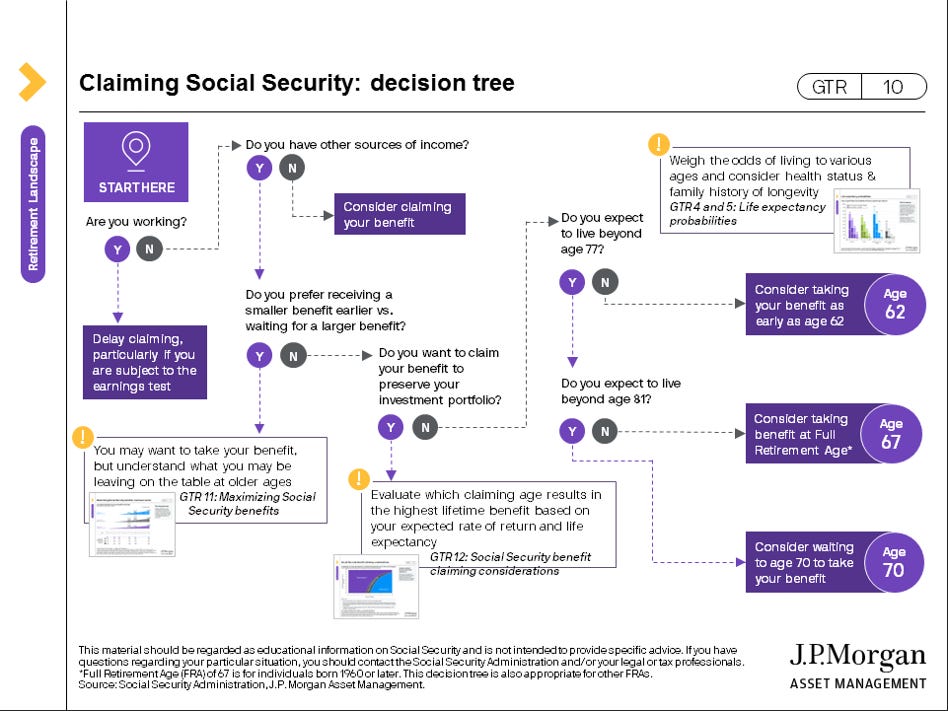

Most of you will be eligible for Social Security retirement benefits. Either from your own work experience or that of a spouse (even former or deceased spouses).

Some of you will also have pension income in retirement, though that is increasingly rare these days.

As you’ll see in the slide above, there are many factors that go into deciding when to claim your Social Security benefits. Many of these are based on how long you expect to live (see life expectancy above).

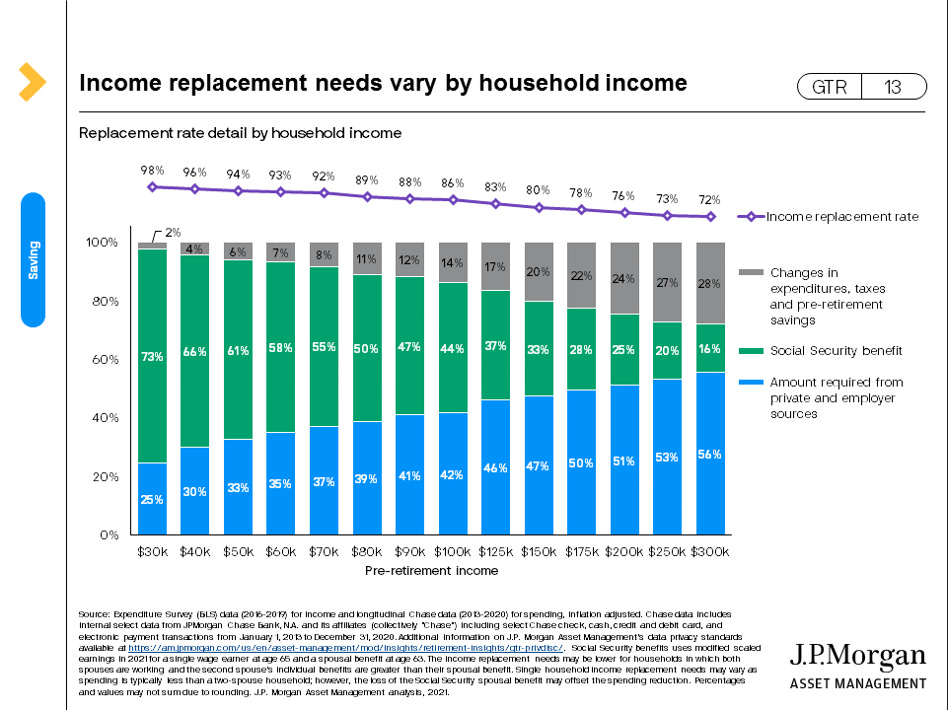

But will your Social Security and/or pension income be enough to support you throughout retirement?

For some of you, it absolutely will.

You can see some estimates of income replacement needs here:

Regardless of your pre-retirement income it’s likely you’ll need to supplement Social Security and other sources of retirement income with additional funds from your accumulated savings and investments.

Saving

In what I hope will come as no surprise, the sooner you start saving, the better.

Time is your biggest ally in planning for your retirement.

But even if you’re in your 50s or 60s and just now starting to plan for your retirement, know that it’s never too late to get started.

You might want to share the slide above with your children, grandchildren, or other younger friends and family who can benefit from getting started right now and benefitting from the power of compound interest over long periods of time.

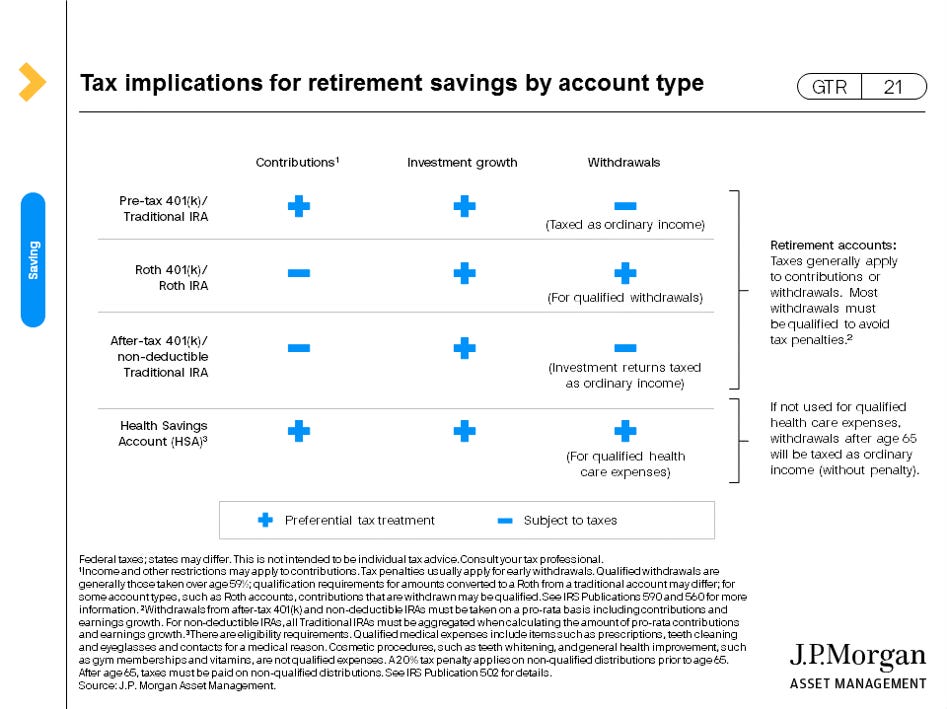

But even if you agree that you should be saving, do you save into your 401k, a Roth IRA, a taxable brokerage account?

Each has its pros and cons:

And any savings is better than no savings.

But it’s best to have a mix of some pre-tax and after-tax savings at a minimum.

If you also have a Roth or HSA account, you’re giving yourself more options and flexibility in the future. Which is always a good thing.

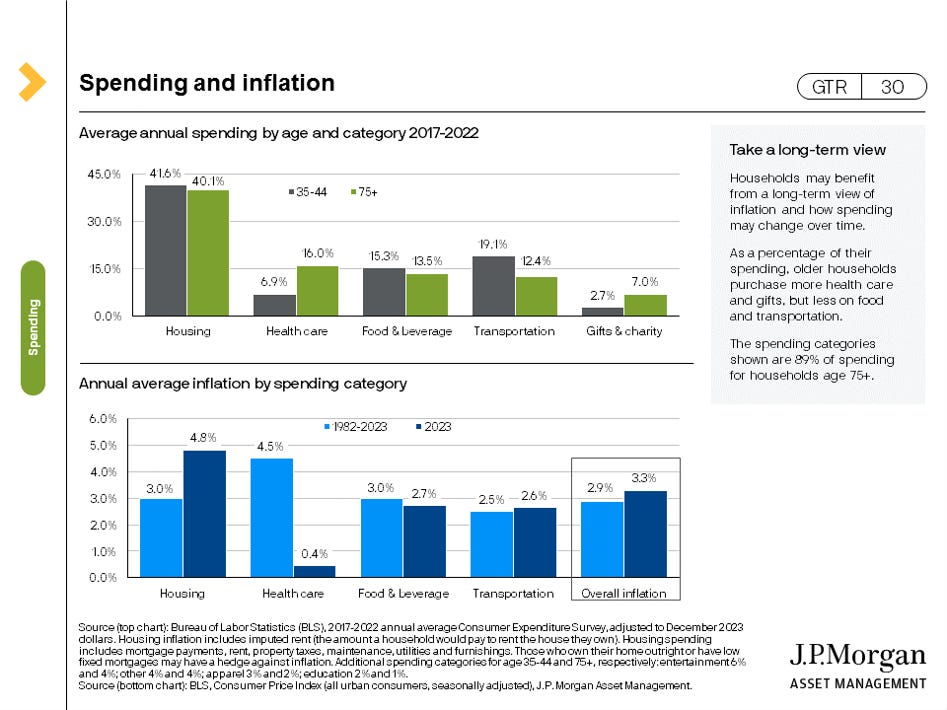

Spending

Through a combination of Social Security, your accumulated savings and investments, and maybe a pension, you’ll need to monitor and manage how much you’re spending.

Should you spend less, so you don’t run out of money?

Or can you spend more, so you don’t die on a mattress stuffed full of money you could have used?

Here’s some average spending figures based on age as well as how inflation impacts different spending categories over time.

And know that even if you have your spending dialed in today, it will evolve over time:

Just last week I wrote about using a tool like Monarch Money to better keep an eye on your spending and overall cash flow.

Investing

Through a combination of longer life expectancies and our lives getting more and more expensive each year due to inflation, just saving your money into a bank account ain’t gonna cut it.

And even though you can get an FDIC-insured money market that’s currently paying 5% interest, that’s not the best solution for the entirety of your retirement years or the entirety of your portfolio.

The good news?

Long-term investing is simple.

If you can just stick with it…

The “sticking with it” part is what makes something so simple not always so easy.

For compounding to work and for time to be your retirement planning ally, you need to create and stick with your investment plan.

Which means you need to create an investment plan that you can stick with.

The creation of your investment plan should only be done in the context of your holistic financial and retirement plan.

Focus

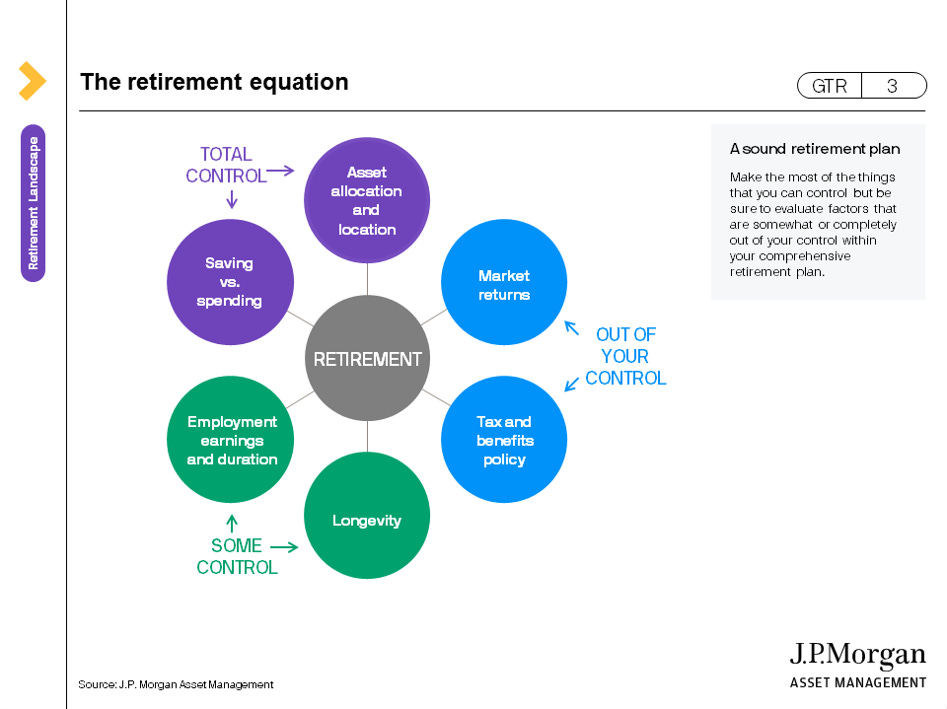

I saved the most important for last:

You need to focus on the things within your control.

Everything else is just noise. Or a distraction.

Yet again, easier said than done.

Because it only takes one distraction to potentially knock your retirement plan - and your life - irretrievably off track.

I work with my clients on all of the above.

And there’s still more to retirement planning…

We also tackle things like:

health insurance

tax planning

making sure your estate plan is up to date and in order

that you have the right risk management tools in place to protect your plan

plus more…

And we need to make sure your money is aligned with who you are and what’s important to you.

What is the single biggest retirement challenge in your mind?

What are you doing to address it?

Hit reply or leave a comment and let me know…

Links & Things

Investing should be boring.

And for me, it is boring.

And I’m not the only one that feels this way:

In case that New York Times link above is paywalled, try this version.

Thoughts? Suggestions?

Hit reply or leave a comment and share your thoughts…

Until next Wednesday,

Russ