Your retirement spending smile

An improved model of your spending throughout retirement

How will you spend money in retirement?

I’m not talking about how much you spend in a week, a month, or even an entire year…

I’m asking what your spending will look like across the 25, 30, or more years you’ll spend in retirement?

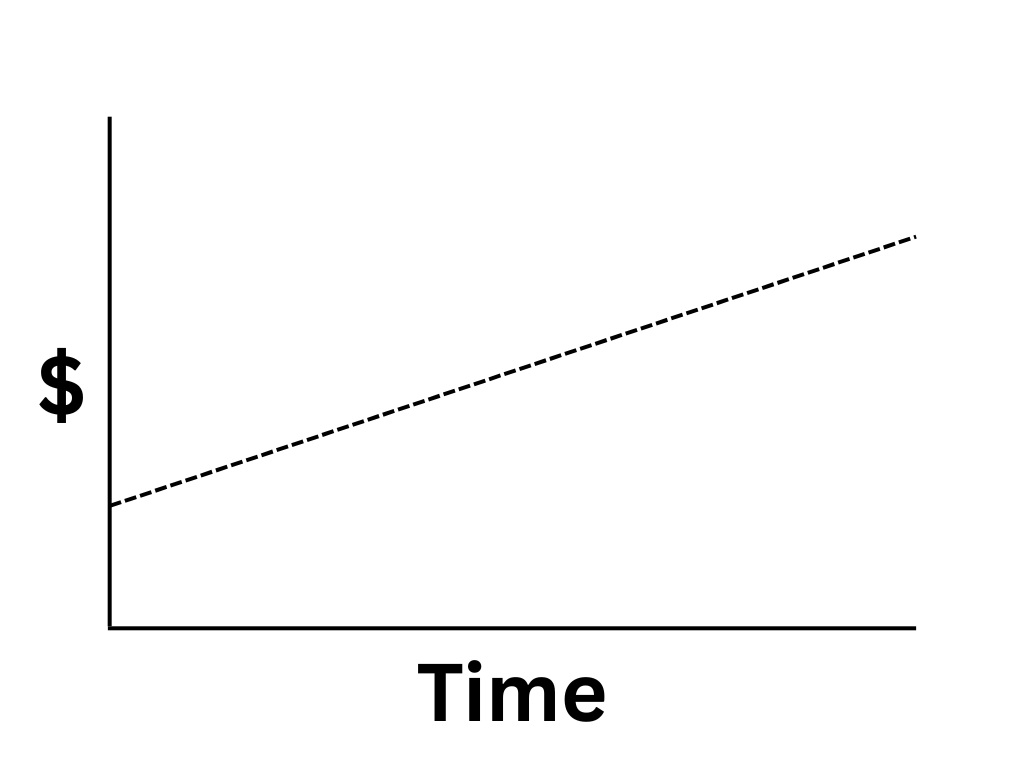

Since the start of my career in the early 90s, everyone agreed that planned retirement spending should be increased annually by an assumed inflation rate.

This was the best way to plan for your retirement spending to keep pace with inflation and the rising cost of living.

It would look something like this:

More recent research over the past 10 years or so argues that this is a flawed assumption for retirement spending.

Referred to as the “retirement spending smile”, research found that retirees' spending typically doesn’t follow a straight line.

Instead, it follows a “smile-shaped” curve over time:

Early Retirement: Spending is higher. Think travel, hobbies, spoiling grandkids, maybe that dream kitchen renovation.

Mid Retirement: Spending often drops—not because folks can’t spend, but because they don’t want to do as much. Travel slows down, routines settle in.

Late Retirement: Spending starts to increase again, driven by healthcare and long-term care costs.

So: higher, then lower, then a bit higher again = the “smile.”

These 3 stages of retirement above are sometimes referred to as your:

Go-go years

Slow-go years

No-go years

As a result, your retirement spending smile might look more like the curved line here:

Another way to think of this spending smile is the green line below.

While it doesn’t look like a smile, it assumes you’re spending a little more earlier in retirement with a more gradual spending increase over time.

Spending a little more of your money earlier in retirement when you’re presumably healthier and more mobile makes sense.

While the numbers absolutely have to work in the context of your plan and your life, it’s also a great strategy to reduce potential regret later in life if you didn’t take that trip or have that experience or spend more time with family and friends.

Here’s what a retirement spending smile looks like for one of my clients in my retirement planning tool:

The retirement spending smile still accounts for inflation, but it also allows for likely spending changes over your retirement.

This spending smile approach is especially well-suited in my retirement planning for women because they:

Live longer than men (often by 3–5 or more years)

Often have lower lifetime earnings, especially if they took time off for caregiving

And may spend more years alone in late retirement

Longer lives make late-in-life healthcare expenses more likely

Any time we’re planning into the future, we’re simply making our best guess about how things will unfold.

The retirement spending smile is simply a guess that best reflects what “typically” happens to spending in retirement.

But you’re not typical, are you?

Whether you (or your advisor) is using fixed annual inflation or the spending smile, these are only 2 among a virtually unlimited number of approaches to planning your retirement spending.

Of course, your retirement plan should also account for health, family history, and other factors that could impact your assumptions and decision making.

It should also account for your personal spending that will best align with you and your lifestyle.

And regardless of which spending model feels best to you, make sure you have the ability to run “what if” scenarios to test different situations and decisions along your life’s journey.

If you have questions about your retirement spending plan or would like to discuss any of this further, please let me know.

With all the “excitement” happening in investment markets recently, it’s a good time to shift your focus from the overall economy to your personal economy.

Instead of worrying about events happening around the country and the world, bring your attention in… to yourself, your family, and the things within your control.

Or, as my friend and colleague Brian recently wrote:

Thanks for reading.

Until next Wednesday,

Russ

This is very interesting! And indeed, makes perfect sense. I'll keep that spending smile in mind when planning my later years.