You need more "and" in your money decisions

Most of your financial choices aren't exclusionary

Good morning,

I’ve spoken about this idea before on my podcast:

The Power of Replacing OR with AND - Episode 14

In today's episode, I want to introduce the idea of replacing the word "or" with "and" when it comes to certain financial decisions. For instance, instead of "invest OR pay off debt", why not "invest AND pay off debt"? I provide 2-3 examples, though there are many more.

And today I’d like to revisit the benefits of making more financial (and life) decisions using the word “and” instead of “or”.

Yes, I’ve written recently about decision making:

Everything in Balance

Happy Wednesday, I’ve shared this quote before: “There are no solutions. There are only trade-offs.” ―Thomas Sowell And this is especially true when you’re planning for your retirement. And your life. The trick is to keep these trade-offs in balance as best you can.

But let’s be a little more specific, shall we?

I was talking with a long-time client couple last week.

We were catching up during a strategy meeting to review their financial plan based on where they are today and what’s ahead in their lives.

One thing that came up was their desire to increase their annual giving to their church to maintain their goal of tithing.

But how best to go about it?

They had essentially 3 options that we discussed:

They could write a check

They could donate directly from one of their IRAs

They could gift appreciated stock from a non-IRA account

Sure, they could also consider a donor-advised fund or other more involved strategies, but for purposes of today’s essay let’s stick to the 3 options listed above.

This will give you a glimpse into how I think about financial decisions in general as well as this specific example.

First, let’s be clear…

Their goal is simply to give more money to their church.

And while I always assume my clients want to make financial decisions in the most tax-efficient manner possible, their primary goal wasn’t to reduce their tax bill.

So why not give money to the church (fulfilling their goal) while also doing so in a tax-friendly manner?

Let’s give money to the church AND save some on taxes.

Not give money OR save some taxes.

There are many opportunities to apply “and” thinking to your money decisions.

To wit…

Pay off debt or invest?

Save for retirement or your kids’ college?

Give money to your family now or leave it after you’re gone?

Spend money today or save for tomorrow?

None of the above are mutually exclusive.

They’re not either-or.

Instead, consider doing some of both.

Like giving to your church and saving on taxes.

So back to my clients…

Write a check

They can afford to write a check direct to their church which would satisfy their goal.

And if they write a check, they can deduct the contribution on their 2024 tax return as an itemized deduction. This assumes they have enough other itemized deductions that all together total greater than the standard deduction.

Note: the standard deduction for 2024 is:

Donate from IRAs

The next option is they could donate to their church directly from an IRA.

And since they’re both over 70.5 years old, this is known as a Qualified Charitable Distribution (QCD).

Money distributed from an IRA is typically taxed as ordinary income.

If they make a donation to a qualified charitable organization directly from their IRA, there’s no income tax paid on the funds.

They can’t deduct the contribution either, but the result is the same.

The client isn’t paying income taxes on the funds coming out of their IRA which they would normally have to do.

Give appreciated stock

The third alternative we discussed was giving appreciated stock from their taxable brokerage account.

Here’s the example I gave them…

Let’s say you own Coca-Cola stock and you originally paid $20 per share.

And let’s say today Coca-Cola stock is worth $60 per share.

If they’ve owned the shares for more than 12 months and they sell the shares, they’ll owe long-term capital gains tax on the difference between their acquisition price ($20) and the current price ($60).

For every share they sell, they’ll owe long-term capital gains on $40 per share.

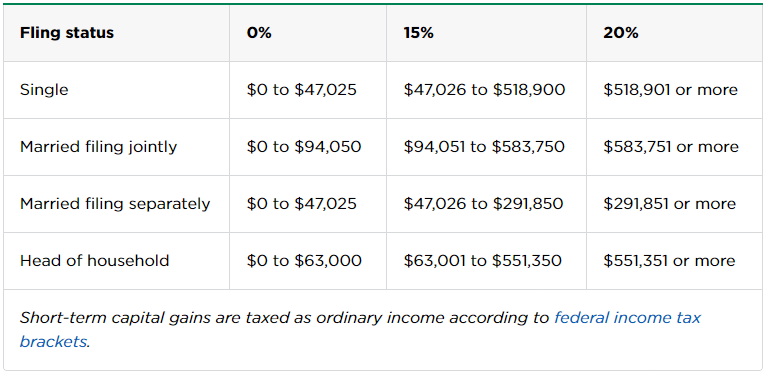

Note: long-term capital gains rates for 2024:

But if they donate this stock to their church they can “give away” the capital gains tax liability to the church who, as a nonprofit, can sell the shares without any capital gains tax.

And the client can still deduct the contribution from their taxes.

But, another goal of this couple is to leave some money behind for their kids and grandkids.

And it’s much more tax-efficient to leave behind assets in a taxable brokerage account than to leave behind assets in an IRA (to a non-spouse beneficiary).

This is due to the “step-up in basis” which I mentioned in this article:

An underappreciated piece of your financial plan

Good Wednesday morning! I’ve written before about multi-tools I own and use like Evernote, a Swiss Army Knife, and a Leatherman Skeletool: These aren’t always the best tool for a specific task I’m working on, but they’re amazingly adaptable and flexible in a variety of situations.

If a non-spouse beneficiary inherits an IRA, they have to take all of the funds out over 10 years and pay income taxes on every penny.

So they asked for my recommendation, and I suggested that they give more out of their IRA as a QCD.

Because otherwise they - or their heirs - will have to eventually pay income taxes on all their IRA assets.

This allows them to:

Give more to their church (achieving their primary goal), AND

Eliminate income taxes on a portion of funds coming out of their IRA, AND

Leave more non-IRA assets to their heirs more tax-efficiently.

And… we also discussed extending their travel goal.

Instead of ending their travel spending when the husband turns 80, we extended it to his 85th birthday.

Sure, sometimes there are some necessary “or” decisions you’ll have to make.

But in my experience, they’re the exception and not the rule.

So look for more opportunities to avoid binary, either-or thinking and instead consider your options to do 2 (or more) things at the same time.

That’s better balance.

And better balance is better living.

Let me know what you think…

Links & Things

I often joke with clients (you know who you are 😉) about the dangers of consuming the “news”.

Shane Parrish agrees with me:

What do you think?

Hit reply or leave a comment and share your thoughts…

Until next Wednesday,

Russ