Your silent partner in retirement

Happy Wednesday!

Did you know that you likely have a silent partner in your retirement planning?

Yep, that's right...

Whether you're single, married, divorced, or widowed, if you have have an IRA, 401k, or other tax-deferred retirement account, you have a silent partner that has a claim to a portion of your account.

And it's the IRS.

Whether you've made pre- or post-tax contributions to your retirement account(s) over the years, the IRS is going to eventually take a portion of your hard-earned savings.

When you begin taking money out of these accounts, when you have to start taking money out of these accounts via Required Minimum Distributions, or both.

To put it in simple term, if you have an IRA that's worth $100,000 and we assume you're in and will forever remain in the 24% Federal income tax bracket, that means that 24% or $24,000 of your $100,000 IRA belongs to the IRS.

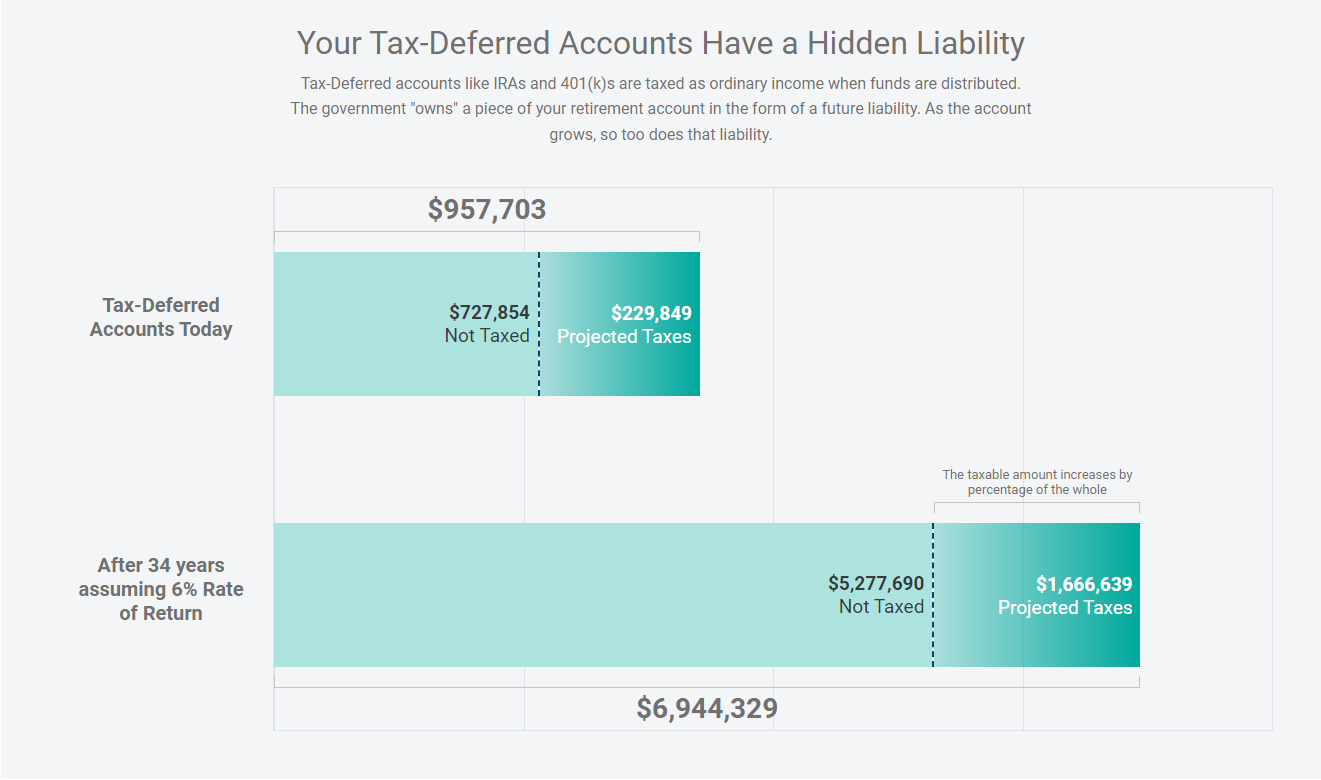

Let's look at a graphic based on our planning in public persona, Lillian Lifestyle...

As you may recall from one of the first videos, Lillian currently has a total of $957,703 in retirement assets between her IRA and 401k.

And Lillian is currently in the 24% Federal income tax bracket.

Here's what this means for her retirement savings:

Source: Holistiplan (click image above to see larger version)

Note: the bottom graphic shows a fixed annual rate of return at 6%. This ain't gonna happen, so it isn't a realistic way to analyze this, which is why we don't rely on fixed rates of return in the big picture planning I provide to my clients.

Nevertheless, I think the graphic above paints a picture of what I'm describing when I refer to the IRS being your silent partner in your retirement.

How do you legally eliminate this silent partner?

Well, one option is you essentially buy them out today.

This is done through a Roth Conversion which involves taking part or all of your IRA, taking the money out, paying income taxes today, and putting the remainder into a Roth IRA.

Why would you do this?

First of all, I'm not sure you would. Or should...

As I've written in the past, I don't buy the strategy that everyone should pursue Roth conversions despite some of my financial advisor colleagues swearing by the practice.

Sure, it might be a good move over time. But then again, maybe not.

It depends on a lot of assumptions:

Future tax rates will be higher than they are currently

The Federal government will forever and always treat Roth IRA balances as they do today

You'll live long enough to recover today's tax liability through portfolio growth

And more...

And while the future is endlessly uncertain, I don't feel comfortable making or recommending that you make assumptions when we don't need to.

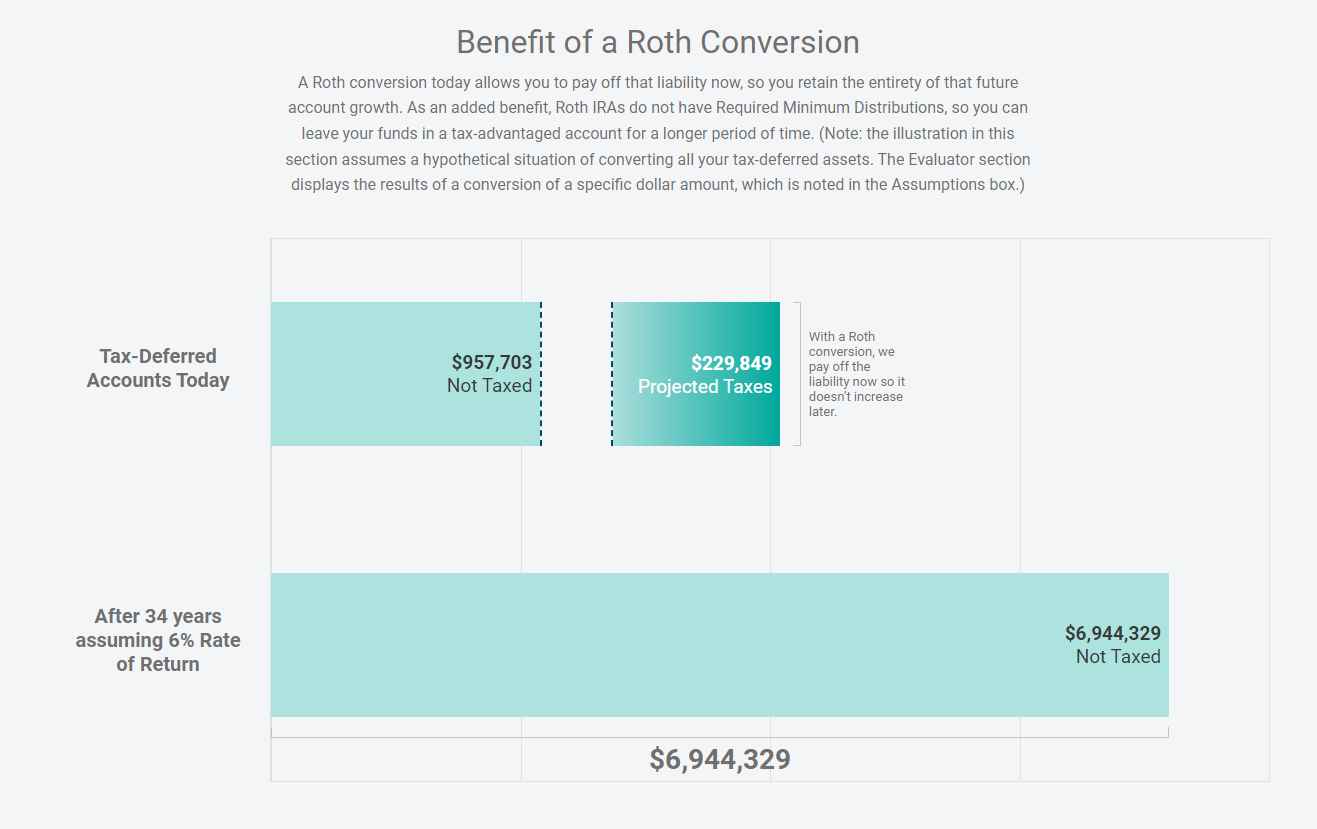

Despite all that, however, here is a graphic that shows the concept of using a Roth conversion to "buy out" your silent partner (the IRS) by paying taxes today:

Source: Holistiplan (click image above to see larger version)

Beyond the tax cost for doing this, the argument is that you'll be in a higher tax bracket in the future because tax rates are historically low at present.

Plus, once you buy the IRS out of your retirement account balance, they don't get the benefit of any future growth in your account.

Do Roth conversions sometimes make sense?

Absolutely!

Do they always make sense, as some advisors would have you believe?

I'm not buying it.

But this week's email isn't about the pros or cons of a Roth conversion.

It's simply to make you aware (or remind you) that you have a silent partner waiting to take a chunk of your retirement account balances.

Be sure you take this into account in your financial planning and lifestyle decisions.

Links & things

As interest rates have risen, many of you have seen the value of your fixed income investments drop in value because bond prices and interest rates move in opposite directions. But did you know that rising interest rates can also lower the value of your lump sum pension option? I've discussed this with a couple of you in the last week or two...

Watch out for:

Thank you, as always, for reading.

And if you have any questions or an idea for a future newsletter, blog post, or YouTube video, I'd love your input.

Just hit reply - I read (and appreciate) every email you send.

Until next Wednesday,

Russ