Comfort in Context

How I define and apply "comfort" in your financial plan

Good morning,

Hope you had a nice Labor Day weekend…

Back in May, I wrote about the possibility that we’re too comfortable and this might be contributing to our tendency to identify what we perceive as problems or challenges.

Michael Easter wrote about this in his book The Comfort Crisis.

I’ve acknowledged that “comfort” is a word I use often in my work.

You can have the best financial strategy, the best investment portfolio, or the best estate plan. But if you’re not comfortable, what have you really accomplished?

Have you just created a new source of stress and worry in your life?

Yes, “comfort” is a subjective concept which will mean something different for each of you.

So today, I’d like to share more about what comfort means to me in the context of your financial planning and money decisions.

To set the stage, let’s first talk about how financial advice is typically delivered…

If you work with a financial advisor and you receive any financial planning at all, it’s often disconnected from your investment strategy.

Most advisors will subject you to a risk tolerance questionnaire.

The problem word here is “tolerance.”

Who wants to “tolerate” anything, especially when it comes to your money?

Not me.

Vanguard has one. So does Schwab.

In fact, a quick Google Search for “investor risk tolerance questionnaire” gives us about 634,000 results.

While neither Vanguard nor Schwab refer to their questionnaires as having to do with “risk tolerance,” make no mistake… that’s precisely what they are.

They’re designed to have you evaluate how much investment risk you think you can tolerate so they can recommend an investment strategy purpose-built to do just that.

To put your portfolio - funded by your hard-earned money - at the maximum risk level you’ve indicated you can stomach.

Not sure about you, but that sounds like the opposite of comfortable to me.

And never mind the fact that your answers to these questions will be completely influenced by your recent investment experiences - good or bad.

My approach is different.

We want to evaluate your “need” to take risk in the context of your financial plan.

I’m honestly not sure how anyone could recommend you make such an important decision based on a short multiple-choice questionnaire.

I could go on for days about the problems with these things.

Just know that they’re created and administered first and foremost to document your attitude toward investment risk to protect your advisor and/or their firm in the event that there’s ever a significant problem between your investment expectations and your investment results.

But wait, there’s more…

Most financial advice is based on active investment management.

This is attempting to outperform the market through superior investment selection and/or market timing.

This strategy simultaneously introduces and ignores another risk.

In an attempt to outperform the market or some arbitrary benchmark, you also run the risk of underperforming the market or benchmark. Sometimes by quite a lot.

OK, I could write volumes about what I see as problems with how most financial advice is delivered. But that’s not my goal today.

Back to comfort…

If you’re a client, many of the following images will look familiar.

In its simplest form, this is how we measure comfort in your financial plan:

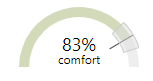

With some context, the above image makes sense. Otherwise, you’re probably scratching your head right about now.

Here’s a different look at the same information:

Again, you can see the number is “83” but with more context, you can see what 83 means relative to some other information.

Here’s another:

Same information, but with more context. This time instead of a percentage score, we’re using dollars.

I’ve written about this before and have even shared some of the above images:

I won’t revisit the overall concept of the comfort zone here. If you’re interested, read the articles linked above.

But I do want to provide a little more background on why it’s called the comfort zone and what that means from a practical perspective.

In my planning work, each client has a personal comfort zone which is defined as a plan “result” between 75% and 90%.

At the lower boundary of your comfort zone, 75% is consistent with a 30-year annualized return of 7.5% for stocks.

In about 25% of all 30-year periods since 1871 have stocks produced a lower return.

Since 1926, a 75% comfort score is consistent with experiencing returns equal to the worst 30-year period in history (sequentially from 1928-1957).

A recommendation within your comfort zone should provide you with confidence (and comfort) that you can reach your goals, even if market performance is poor in the future.

Conversely, a score of 95% indicates a confidence level where client goals are exceeded in all but the lowest 5% of simulated returns and would even survive a great depression average return.

Of course, as I’ve written many, many times before, your financial plan - and your comfort zone - are merely a snapshot in time. They’re based on what we know right now. They aren’t a forecast or prognostication about the future.

So naturally your comfort zone and your overall financial plan can and will change over time.

Which is why it’s smart to regularly review and update your comfort zone to make sure your plan is still on track. Or make small adjustments along the way to get it back on track.

But if your personal plan has a score of 83 as in the images above, what does that mean exactly?

Many advisors who use a similar approach to stress-test your plan might refer to this as an 83% probability of success and a corresponding 17% probability of failure.

But that’s misleading at best.

Plans don’t fail.

Remember our friends Thelma & Louise?

If you’re heading the wrong direction, simply turn the wheel and adjust your course.

The same applies with your comfort zone and your financial plan. Which is why we regularly review your plan and make small adjustments - or course corrections - as we go.

In this context, a plan score of 83 is better described as an 83% probability of excess (exceeding your goals) and a 17% probability of adjustment which means the likelihood you’ll need to adjust your plan over time.

In life - and in your financial plan - there is such a thing as too much comfort.

And while we’re measuring and addressing that in your financial plan, we want to make sure we’re not ignoring what’s comfortable to you and instead are creating a strategy that’s merely “tolerable.”

What do you think?

Hit reply and share your thoughts…

Links & Things

What do you really want?

Are you sure about that?

I’ve written about this before.

Encourage you to watch this:

Selling Your Home?

If you or someone you know is selling a home, this resource might be helpful:

Thank You!

I’m grateful to have you as a reader.

If you have any questions or an idea for a future newsletter, blog post, or YouTube video, I'd love your input.

Just hit reply - I read (and truly appreciate) every email you send.

Until next Wednesday,

Russ