Is your retirement income plan resilient?

You want reliable retirement income no matter what

Whether you’re 2 years, 2 months, or 2 days away from retirement, what do you do when:

The investment markets drop

Inflation starts going up

Interest rates rise

There’s a new military conflict somewhere

Tariffs

You name it…

I’m confident no one wants to retire into heightened uncertainty.

But guess what?

Uncertainty will be your constant companion leading up to and throughout your retirement years.

Sure, sometimes the uncertainty gets dialed up to 11 and other times it’s background noise.

But it’s always there.

That’s why I believe it’s important to regularly stress test your retirement income plan and see how it holds up against an utterly unknowable future.

Here’s a retirement income plan summary for a hypothetical client named Jane:

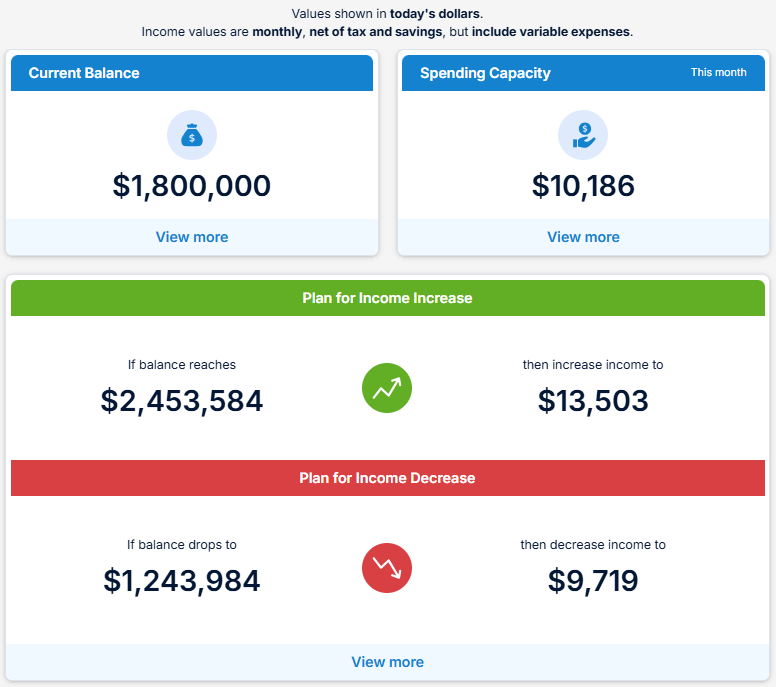

Jane’s current investment portfolio is in the upper left at $1.8 million.

Her achievable spending level is shown in the upper right at $8,443 after-tax for this month.

The green and red shows her retirement spending guardrails.

The guardrails tell us:

If her portfolio were to fall from $1.8 million to $1.223 million or less (about a 32% drop), her monthly after-tax spending would need to adjust from $8,443 to $8,041 per month. A reduction of $402, or about 5% of her current spending number.

And if her portfolio were to rise to a value of $2,125 million or more (an 18% increase), Jane could increase her monthly spending by 17%, or $1,454.

Here’s a better visual of how these guardrails set expectations in Jane’s retirement income plan:

There’s a lot of data and calculations that go into the numbers above, including Jane’s Social Security benefit, her age, her life expectancy, and more.

But how reliable are these numbers?

And what happens when - not if - the stock market drops?

Especially if you’re on the doorstep of retirement!

We’ve already begun to demonstrate how much Jane will need to adjust her monthly spending if her personal portfolio - not the market - goes up or down by a certain amount.

But what about 10, 20, or more years from now?

How can we test if this plan will hold up for the entirety of Jane’s retirement when we have no clue what the future will look like?

Well, we have a couple of options…

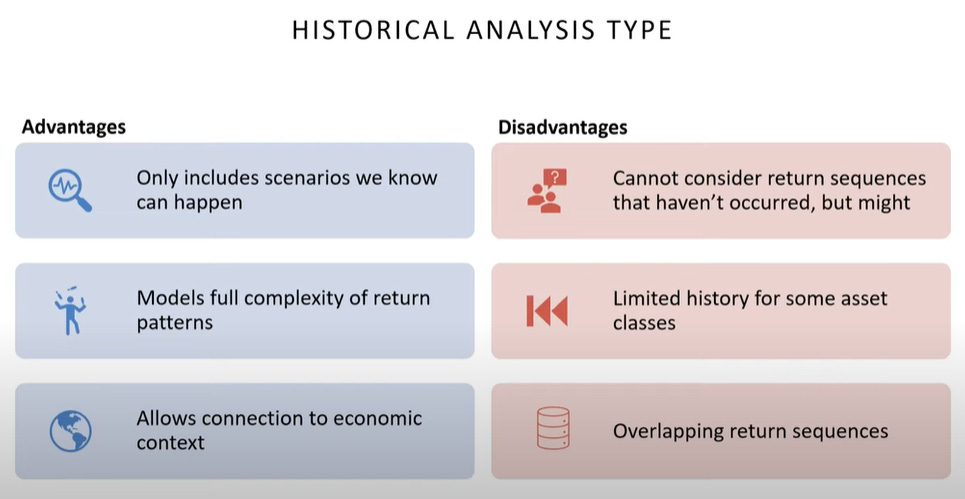

In the plan above, I used an “Historical” stress test:

As the name implies, this stress test uses historical sequences of returns and inflation to model sequence-of-returns and sequence-of-inflation risk.

In other words, we’re analyzing how Jane’s retirement income plan would have held up in the face of what we’ve actually experienced before.

This includes the Great Depression, several recessions, 2 world wars, and literally everything else that’s happened to our families over the generations.

Of course, with any model or set of assumptions, there are pros and cons:

Here’s another look at Jane’s retirement income plan:

It uses all the same data, but instead of a historical stress test, we’re using something called a “Traditional Monte Carlo” stress test.

Traditional Monte Carlo creates simulated sequences of returns and inflation using a single set of return assumptions.

This stress test models what might happen in the future regardless of whether it’s happened in the past.

While Monte Carlo simulations can model much worse markets than we’ve ever experienced (think back-to-back-to-back Great Depressions), it can also model much better markets than we’ve ever experienced as well.

Here are the pros and cons of Monte Carlo stress tests:

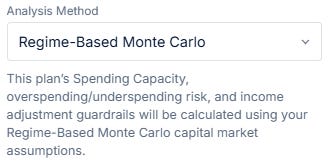

And finally we can also utilize a “Regime-Based Monte Carlo” stress test:

Here’s Jane’s retirement income plan using this stress test:

Instead of using a single set of assumptions like Traditional Monte Carlo, Regime-Based Monte Carlo uses 2 sets of return and inflation assumptions, one for the near-term and one for the long-term.

Whether Traditional or Regime-Based, it’s still Monte Carlo and will share similar pros and cons.

Here’s a little more on each of the 2 flavors of Monte Carlo stress tests:

While each of these 3 stress tests has value in evaluating the reliability of your retirement income plan, I like Historical the best and use it most often for my clients.

And for myself.

The primary benefit of Historical is that we’re using numbers we’ve already experienced in the past.

We’re not relying on someone’s assumptions about what stocks, bonds, cash, and inflation “might” do in the future.

Because if anyone is making an assumption about the future, they’re going to be wrong.

You can’t avoid this because, well… it’s the future.

And if we do want to look at Monte Carlo to provide another perspective on your retirement income plan, I’m not a fan of Regime-Based.

Regime-Based introduces not just one, but two sets of assumptions about the future.

That’s 2 sets of guesses about how the future might look.

Which means that’s 2 opportunities to be wrong.

No thank you.

Is Historical stress testing the best?

Nope.

We’re talking about the future here.

The unknowable, unseeable future.

The best we can do is chart a course into the unknown and make course corrections as needed along the way.

And as I’ve written before,

But it can be a helpful decision making tool.

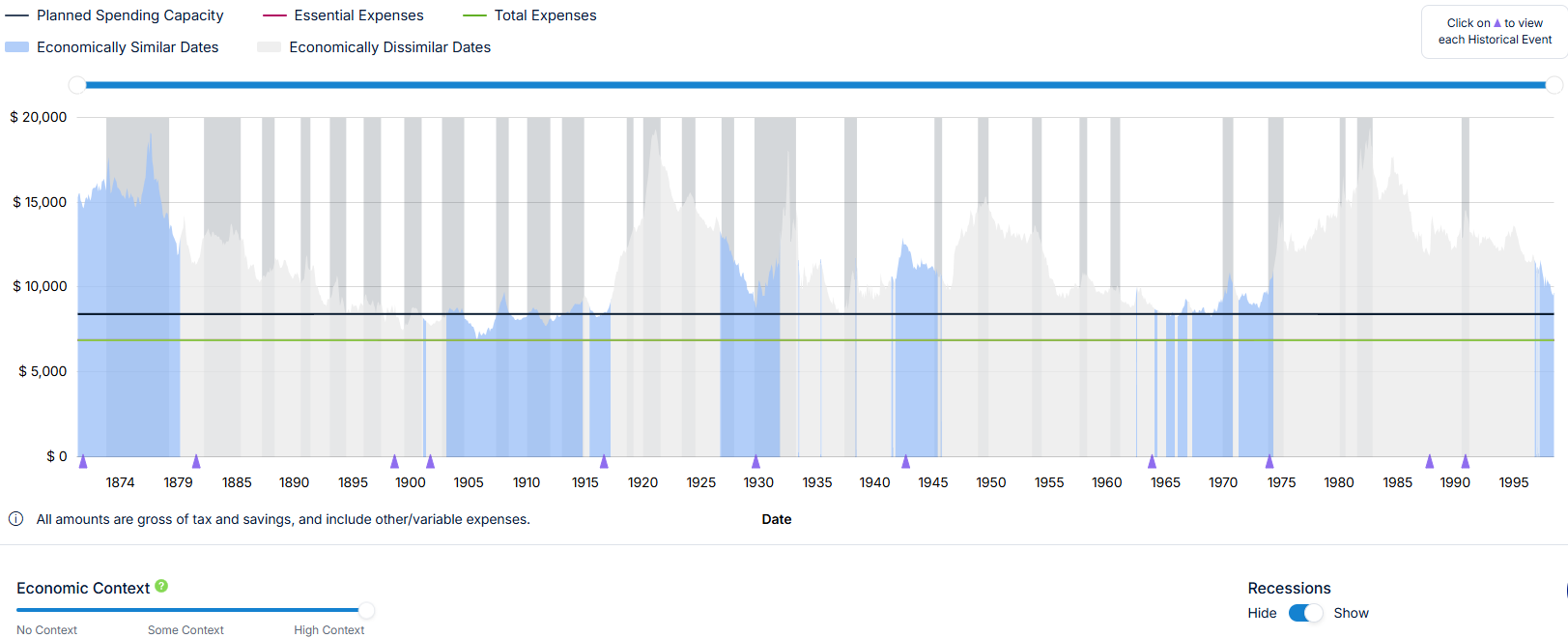

In addition to the stress testing models above, I think this chart offers a helpful perspective (click the image for larger version):

This chart shows how Jane’s achievable retirement spending level (in today’s dollars) would have held up in every month going all the way back to 1871.

The horizontal black line is what she can afford to spend.

The horizontal green line is what she needs to spend.

And the blue and grey chart in the background shows what Jane’s monthly historical spending capacity would have been at each point in history.

Here’s the same chart but I’ve set it to show all past recessions, highlighted by the grey vertical bars:

Below is Jane’s Historical Analysis chart zoomed in for the years 1929 to 1941 which was The Great Depression:

As you can see in the chart above, both Jane’s achievable spending and necessary spending (funded by her retirement paycheck) would have held up really well throughout one of the darkest periods in our country’s financial history.

So whether your retirement is right around the corner or you’ve been retired for a few years already, tools like the these can help provide comfort and clarity in the face of increased uncertainty.

The combination of retirement income guardrails, retirement income stress tests, and seeing how your retirement spending would have held over the past 150 years will hopefully provide some much needed peace of mind when it might feel like the world is falling to pieces around you.

And these are just a few of the tools in my retirement planning toolbox.

Combined with my 30+ years of experience delivering financial advice, I’m confident in my ability to help you navigate retirement.

Especially when the going gets rough.

Wanted to share this timely read and reminder from Adam Grossman.

I think his 7 lessons are worth reviewing and taking to heart, especially #4:

Please give it a read and let me know what you think with all that’s going on these days…

Thank you for reading.

Until next Wednesday,

Russ